Published: 21st Oct, 2019

India is on track to achieve 175 GW of renewable energy by 2022.

Issue

Context

India is on track to achieve 175 GW of renewable energy by 2022.

Background

- Power is one of the most critical components of infrastructure crucial for the economic growth and welfare of nations.

- India’s power sector is one of the most diversified in the world with thermal coal/gas constituting 66%, nuclear 2%, renewables 13%, and hydro power 19% of installed capacity.

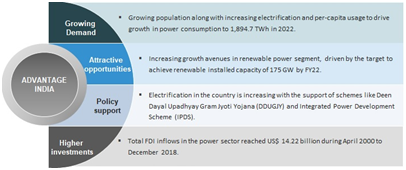

- Electricity demand in the country has increased rapidly and is expected to rise further in the years to come. In order to meet the increasing demand for electricity in the country, massive addition to the installed generating capacity is required.

- In May 2018, India is ranked 4th in the Asia Pacific region out of 25 nations on an index that measures their overall power.

- India is the third largest producer and the third largest consumer of electricity in the world. Electricity production reached 339.14 Billion Units in FY20 (As of June 19). India is ranked 4th in wind power, 5th in solar power and 5th in renewable power installed capacity as of 2018.

Analysis

Market Size

- Sustained economic growth continues to drive electricity demand in India.

- ‘Power for all’ scheme has accelerated capacity addition in the country. At the same time, the competitive intensity is increasing at both the market and supply sides.

- Total installed power capacity in India is 356 Gigawatt (GW) (as of May 2019).

- In recent years, the major growth drivers have been renewable energy sources such as solar and wind power, and investment from the private sector.

- For the last three years, growth in generation from renewables has been close to 25%. India aims to have a renewables capacity of 175 GW by 2022 and 500 GW by 2030.

Investments in Power Sector

- The private sector accounts for almost half the installed generation capacity.

- Thermal plant capacities are large and therefore targeted capacity additions can be achieved by constructing fewer such plants. On average, it would take 18 solar or wind projects to generate the same quantity of power as one thermal plant. For the same reason, switching from fossil fuel to renewables will remain challenging as the administrative overheads that would have to be incurred in setting up the multiple projects could significantly add to the cost.

- As the capacity of power plants increases, the average cost of power per MW reduces. The average cost per MW for a thermal plant is about 25% lower than that of a solar plant. In order to surmount the cost advantages that large thermal plants enjoy today, we must focus on developing larger solar and wind power plants that can also exploit similar economies of scale.

Challenges for Power Sector

- Power deficit: Some of the issues leading to the power deficit situation in the country include

- Shortage of fuel,

- High Aggregate and commercial (AT&C) losses,

- A differential tariff structure

- Delays in tariff revisions.

High AT&C losses and losses arising due to issues with tariff affect the ability of distribution companies (discoms) to buy power to supply to the consumers.

- Generation capacity increasing, but utilization of generation capacity is still low:

- Historically, inadequate generation capacity was the key contributor to power deficit. However, generation capacity has improved in the last few years due to high participation by the private sector.

- Over the years, the capacity to generate electricity has increased, however the actual generation of electricity has not been commensurate with this increased capacity. Key reasons for the low utilization of generation capacity are: (i) shortage of fuel, especially coal, and (ii) unviable Power Purchase Agreements.

- The coal sector has failed to match production with the growth in coal-based generation capacity. This has created a gap between the demand and supply of coal. As a result, India’s coal imports have risen from 59 to 168 million tonnes from 2008-09 to 2013-14 (185%). Shortage of coal affects the generation of power, leading to power deficits.

- Aggregate Technical and Commercial (AT&C) loss:

- The Accelerated Power Development Program was launched in 2002-03 with the main objective of reducing AT&C losses. However, reduction in AT&C losses (1.1% per annum) has been slower than the target (3% for utilities with losses above 30%; 1.5% for others).

|

- Differential tariff, delays in tariff revisions lead to financial losses

- The differential tariffs for commercial, industrial and agricultural consumers are prevalent in India due to direct subsidies received from the state government and cross-subsidisation by commercial and industrial consumers.

- Supplying electricity at tariff lower than the cost to supply, along with delay in tariff revisions has led to discoms facing huge financial losses.

- Borrowings by state owned discoms has been increasing

-

- The accumulated losses of state-owned discoms (without subsidies) rose from Rs 11,699 crore in 2004-05 to Rs 71,271 crore in 2013-14. These losses have resulted in state discoms relying more on short-term loans to fund their operations.

- Consequently, the interest cost on these loans worsens the poor finances of state discoms. Poor finances of the discoms affect their ability to buy power, thus leading to power deficits.

- Renewable energy pricing per unit is costly

-

- The thermal power is still cheaper than renewable power due to the small size and huge costs of renewable power plants.

- The implementation of intended nationally determined goals under Paris climate Agreement requires India to shift from thermal to renewable power.

- Efficient Power storage technology not available

- India is not having the efficient power storage technology. There are four types of approaches adopted towards power saving in the world:

- Batteries– a range of electrochemical storage solutions, including advanced chemistry batteries, flow batteries, and capacitors

- Thermal– capturing heat and cold to create energy on demand or offset energy needs

- Mechanical Storage– other innovative technologies to harness kinetic or gravitational energy to store electricity

- Solar cells – converts sunlight into electricity.

- Hydrogen– excess electricity generation can be converted into hydrogen via electrolysis and stored

- Pumped Hydropower– creating large-scale reservoirs of energy with water

- India is not having the efficient power storage technology. There are four types of approaches adopted towards power saving in the world:

Government Initiatives for promoting Power Sector

The Government of India has identified power sector as a key sector of focus so as to promote sustained industrial growth. Some initiatives by the Government of India to boost the Indian power sector:

- Structural changes in the regulatory framework:

- The power sector in an economy is typically broken into three segments: Generation, transmission and distribution. These three segments and power trading are regulated in India under a consolidated and modernized Electricity Act of 2003.

- A draft amendment to Electricity Act, 2003 has been introduced. It discusses separation of content & carriage, direct benefit transfer of subsidy, 24*7 Power supply is an obligation, penalisation on violation of PPA, setting up Smart Meter and Prepaid Meters along with regulations related to the same.

- Ujwal Discoms Assurance Yojana (UDAY):

- It was launched by the Government of India to encourage operational and financial turnaround of State-owned Power Distribution Companies (DISCOMS), with an aim to reduce Aggregate Technical & Commercial (AT&C) losses to 15 per cent by FY19.

- The power deficit situation in the country has improved in the past few years. From 2008 to 2014, energy deficit (shortfall in energy supply during a day) has reduced from 11.0% to 3.6% and peak deficit (shortfall in supply during highest consumption period in a day) has reduced from 11.9% to 4.7%.

- Power tariffs: As of August 2018, the Ministry of New and Renewable Energy set solar power tariff caps at Rs 2.50 (US$ 0.04) and Rs 2.68 (US$ 0.04) unit for developers using domestic and imported solar cells and modules, respectively.

- National Policy on Biofuels-2018: The Government of India approved National Policy on Biofuels – 2018, the expected benefits of this policy are health benefits, cleaner environment, employment generation, reduced import dependency, boost to infrastructural investment in rural areas and additional income to farmers.

Way Forward

India aims to have a renewables capacity of 175 GW by 2022 and 500 GW by 2030. Solar and wind power plants would account for much of the targeted capacity from renewables. How can this be achieved? A cost-effective way to power generation is the key:

- Create generation assets with the lowest unit cost by optimising plant capacities and encouraging private sector investment.

- Build large capacity plants so that cost-effective power generation is realized

- Declining marginal cost for capacity provides opportunities for replacing existing capacity with newer capacity that are more efficient.