Published: 10th Jan, 2019

Union Cabinet approved amalgamation of Bank of Baroda, Vijaya Bank and Dena Bank. Every permanent and regular employee of the transferor banks (Vijaya Bank, Dena Bank) will become an employee and will hold his/her office therein in the transferee bank (Bank of Baroda).

Issue

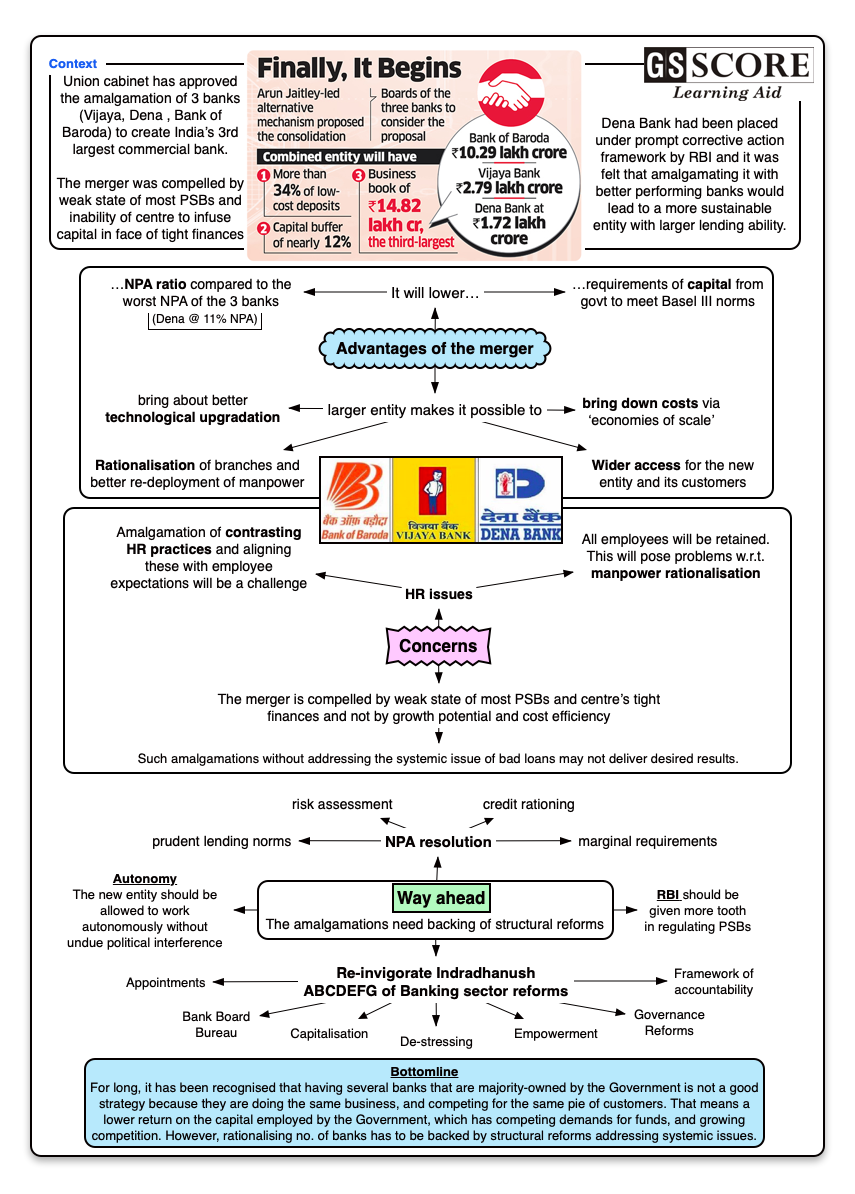

Context:

- Union Cabinet approved amalgamation of Bank of Baroda, Vijaya Bank and Dena Bank. Every permanent and regular employee of the transferor banks (Vijaya Bank, Dena Bank) will become an employee and will hold his/her office therein in the transferee bank (Bank of Baroda).

- The merger of Bank of Baroda, Vijaya Bank and Dena Bank will create the third largest lender in the country, with advances and deposits market share of 6.9% and 7.4%, The new merged entity will overtake ICICI Bank as India’s third largest commercial bank after SBI and HDFC Bank.

- The government owns majority stakes in 21 lenders, which account for more than two-thirds of banking assets in the Asia’s third biggest economy. But these PSU banks also account for the lion’s share of bad loans or NPAs plaguing the sector and need crores of rupees in new capital in the next two years to meet global Basel III capital norms.

About:

- Under Basel III, a bank's tier 1 and tier 2 capital must be at least 8% of its risk-weighted assets. The minimum capital adequacy ratio (CAR) (including the capital conservation buffer) is 10.5%. The merged entity will have CAR of 12.5%

- Dena Bank’s capital adequacy ratio stood at 10.1% on 30 September, Vijaya Bank’s at 13.56% and Bank of Baroda’s at 11.88%. The branch network of the combined entity will be close to 9,500.

- While Dena Bank has been placed under the Prompt Corrective Action (PCA) framework by the Reserve Bank of India, with restrictions on lending, Vijaya Bank is among the only two state-run lenders to have reported a profit in 2017-18.

- The government owns 68.77% in Vijaya Bank, 80.74% in Dena Bank and 63.74% in Bank of Baroda.

- This amalgamation/merger is based on Share swap ratio. Shareholders of Vijaya Bank and Dena Bank could get 402 and 110 equity shares of Bank of Baroda for every 1,000 shares they held. The share swap ratio has taken into account how Dena Bank has performed in the past couple of years, with bad loans ballooning to 23.64% in the September quarter, compared with 5.86% and 11.78% of Vijaya Bank and Bank of Baroda, respectively.

Background:

- The government has been working within the Four “R” philosophy in the banking sector:

- Recognition of bad assets,

- Resolution of the assets (via Insolvency and Bankruptcy Code),

- Recapitalization (2.1 lakh crore assured in October 2017) and

- Reform (utilize this limited capital and infuse it prudentially to create a strong structure).

- Only a stronger bank can utilize the asset being pumped in. Stronger bank has following characteristics:

- Autonomous functioning,

- prudential lending,

- accountable leadership (to shareholders),

- has high risk weighed buffer,

- meets international norms (like basel3).

Analysis

- Countries having much larger economies than India have far fewer banks.

- In the wake of mounting NPA, Bank lending was weak hurting corporate sector investment. This is because the corporate sector investment model is Credit led.

- Mere amalgamation of banks will not provide solution to NPA problem. This problem will primarily be tackled by Insolvency and Bankruptcy resolutions. But there has to be “competition” in this area as well.

- As of now only 3-4 people/entities come for resolution/auction plan under Insolvency and Bankruptcy Code. This forces banks to undertake huge haircuts (discounted debt sale).

Why these three banks were chosen for merger?

- These banks initially emerged as regional players.

- Vijaya Bank: It basically operates in South India, is smaller in size but has healthy financial status.

- Dena Bank: It started its operation from Bombay (basically, a Western India Bank). It is under RBI’s PCA regulation ( sign of unhealthy financially status)

- Bank of Baroda: It started operations from Gujarat. It is not strong in SME and retail lending and is also not having much presence in South as Vijaya Bank has.

Is this a merger or an amalgamation?

- Merger: like structured (complementarity) entities combine with each other (Business necessity – ING Vyasa and Kotak Mahindra Bank). Example: merger of SBI with its 5 subsidiaries.

- Amalgamation: 3 banks will combine to create a 4th bank with a new logo and operational standard. Easy for government to make way as it is a majority shareholder in all these three banks.

- NPA/liabilities in descending order : Dena Bank, Bank of Baroda, Vijaya Bank

- If these banks had been kept alive. Govt would have had to infuse fresh capitals to meet Basel 3 norms.

- Now with merger/amalgamation: bank board of this newly created amalgamated entity will have to decide on ways to meet Basel 3 capitalization standard.

- Since this amalgamation will give the government enough room to “move away” from recapitalization requirement, this “merger/amalgamation” can be better termed as amalgamation of balance sheet.

Some important pointers

- If Government doesn’t bail these entities out, there would be less burden on taxpayer, more revenue available with the Govt to spend on welfare measures.

- Govt could have avoided this amalgamation in an election year. Trade unions and other political outfits are already opposing this move.

- Govt has mentioned that approx. 85K employees will be retained. This will cost this new entity dearly as an amalgamated/merged entity requires manpower rationalization and work procedure re-standardization. If every employee is retained, revenue expenditure will rise. In this IT age, much of the banking transactions are anyhow happening online – keeping all branches of each and every amalgamated entity will not be a prudent decision.

Action plan and challenges foreseen:

- Rationalization of branch and manpower: All India bank employee’s association has already anticipated this rationalization. Regional headquarters and branches of these three entities are bound to go on a rationalization drive to remain financially viable.

- Timeline for completion of amalgamation: 4-6 months. This is different than SBI merger because those entities were virtually SBI in different avatars. Bank of Baroda, Vijaya Bank and Dena Bank – all have different operational standards, manpower policies and area of expertise /functionalities.

- Also the pay and allowance offered to the employees/officers of transferor banks will not be less favorable as compared to what they would have drawn in the respective transferor bank. This will greatly add up to the revenue burden, thus increasing cost of operations.

- Consolidation is another option to go for (instead of privatization). But it will require cleaning of balance sheets and removal of operational bottlenecks. This consolidation didn’t precede amalgamation. Dena Bank has higher share of NPA and is also under PCA. When the news of amalgamation reached sharemarket, share stock value of Dena Bank rose but that of Bank of Baroda fell.

- All these three banks are listed and hence amalgamation must take into account “investor’s sentiment.

- Department of Financial Services (DFS) decides on higher leadership selection in PSB. RBI does not have power to decide on possible actions that can be taken on “errand” directors/CEO of these PSB.

Way forward:

- NPA resolution: Prudent lending norms, risk assessment, Credit rationing and marginal requirements can help in tackling NPA. Bank Consolidation/amalgamation and merger should be seen merely one of many options available, but not the primary one.

- Narsimhan committee had recommended reduction of Govt shareholding (Equity) in Public Sector Banks (PSB) from 51 to 33%. As an added measure, it would be good to abolish Department of Financial Services (DFS).

- Time to dodge down “double accountability trap”. As of now PSB management board is not clear of its governance structure and regulatory structure (DFC and RBI).

- A Possible re-alignment in regulation: Let RBI manage PSBs instead of DFS (ministry of Finance) as DFS did perform a great role during bank nationalization.

- Post amalgamation, next step should be to allow this newly created entity to work autonomously (managerial freedom) and avoid political interference.

- Re-invigorate Indradhanush- A.B.C.D.E.F.G of Banking Sector Reforms (Appointments, Bank Board Bureau (BBB), Capitalization, De- Stressing,Empowerment, Framework of accountability and Governance reforms).

Learning Aid

Practice Question:

If Bank of Baroda, Vijaya Bank and Dena Bank would have been kept alive, government would have had to infuse fresh capitals to help them meet Basel III norms. Under this context, is this amalgamation move a “merger” or an attempt to amalgamate balance sheet?