12th July 2022 (7 Topics)

1

Jul

2

Jul

4

Jul

5

Jul

6

Jul

7

Jul

8

Jul

9

Jul

11

Jul

12

Jul

13

Jul

14

Jul

15

Jul

16

Jul

18

Jul

19

Jul

20

Jul

21

Jul

22

Jul

23

Jul

25

Jul

26

Jul

27

Jul

28

Jul

29

Jul

30

Jul

Sarfaesi Act, invoked against telecom provider GTL

Context

Banks have invoked the Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest (SARFAESI) Act against telecom infrastructure provider GTL to recover their pending dues.

- The recovery action has been initiated by IDBI Bank on behalf of lenders, whose total exposure to GTL stood at Rs 7,250 crore as of December, 2021.

About

SARFAESI Act:

- The SARFAESI Act of 2002 was brought in to guard financial institutions against loan defaulters.

- To recover their bad debts, the banks under this law can take control of securities pledged against the loan, manage or sell them to recover dues without court intervention.

- The law is applicable throughout the country and covers all assets, movable or immovable, promised as security to the lender.

Elements of the SARFAESI Act:

The SARFAESI Act is applied to the entire country of India. The SARFAESI Act, 2002 provisions are in effect for modifying the four laws listed below:

- Indian Stamp Act, 1899.

- The recovery of the debts due to the Banks and Financial Institutions Act, 1993 (RDDBFI).

- The Depositories Act, 1996 and for those matters that are connected therewith or incidental thereto.

- The Reconstruction and Securitisation of Financial Assets and Enforcement of Security Interest Act, 2002.

Aim of the SARFAESI Act:

The SARFAESI Act has two main objectives:

- Recovering the financial institutions’ and banks’ non-performing assets (NPAs) in a timely and effective manner.

- Allows financial organisations and banks to sell residential and commercial assets at auction if a borrower defaults on his or her debt.

Need for the SARFAESI Act

- Before the law was enacted in December 2002, banks and other financial institutions were forced to take a lengthy route to recover their bad debts.

- The lenders would appeal in civil courts or designated tribunals to get hold of ‘security interests’ to recovery of defaulting loans, which in turn made the recovery slow and added to the growing list of lender’s non-performing assets.

- Recognising that one out of every five borrowers is a defaulter, the government was under obligation to provide proper mechanisms for debt recovery as well as to foreclose the security.

- Hence, The SARFAESI Act, 2002 (the Securitisation Act) attempts to fulfil these dual goals, as well as to provide a wide legal framework for asset Securitisation and asset reconstruction.

What powers do banks have under the law?

- The Act comes into play if a borrower defaults on his or her payments for more than six months.

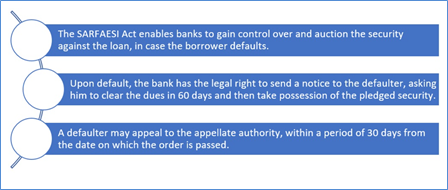

- The lender then can send a notice to the borrower to clear the dues within 60 days.

- In case that doesn’t happen, the financial institution has the right to take possession of the secured assets and sell, transfer or manage them.

- The defaulter, meanwhile, has recourse to move an appellate authority set up under the law within 30 days of receiving a notice from the lender.

- According to a 2020 Supreme Court judgment, co-operative banks can also invoke SARFAESI Act.

- According to the Finance Ministry, the non-banking financial companies (NBFCs) can initiate recovery in Rs. 20 lakh loan default cases.