23th September 2025 (13 Topics)

1

Sep

2

Sep

3

Sep

4

Sep

5

Sep

6

Sep

8

Sep

9

Sep

10

Sep

11

Sep

12

Sep

13

Sep

15

Sep

16

Sep

17

Sep

18

Sep

19

Sep

20

Sep

22

Sep

23

Sep

24

Sep

25

Sep

26

Sep

27

Sep

29

Sep

30

Sep

GST 2.0 Rate Rationalisation

Context:

The Government has undertaken a major GST rate rejig to simplify classification, rationalise slabs, and reduce the inverted duty structure (IDS), with the aim of boosting consumption and investments.

Background of GST Rationalisation

- Introduction of GST (2017): GST subsumed 17 indirect taxes and 13 cesses into a unified framework, initially with four slabs – 5%, 12%, 18%, and 28%.

- Problem of Complexity: Multiple slabs and exceptions created confusion for taxpayers and businesses.

- Objective of GST 2.0: To streamline rates, reduce disputes, and spur consumption by placing items in a simplified two-slab structure.

Key Changes in Rate Structure

- Standardisation of Rates:

- Four main slabs (5%, 12%, 18%, 28%) further rationalised; exemptions removed for items like bread, food additives, and health insurance.

- Precious stones taxed at 1.5%; diamonds at 0.25%; gold and silver at 3%.

- Medical devices, bio-fuel, and hydrogen vehicles rationalised under lower slabs.

- Consumer Impact:

- Household expenditure expected to decline due to reduction in rates of essential goods like milk products, footwear, and packaged food.

- Some items such as tobacco continue to be taxed at higher rates for revenue and health concerns.

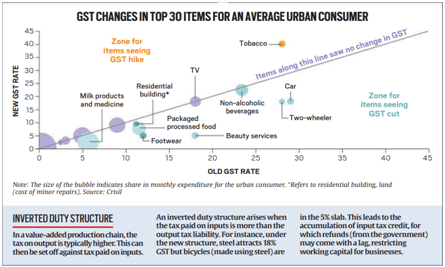

Inverted Duty Structure (IDS): A Persistent Issue

- Definition: IDS arises when input tax is higher than output tax, leading to accumulation of Input Tax Credit (ITC).

- Examples: Steel taxed at 18% but bicycles made using steel at 12%.

- Concerns: Refunds are often delayed, locking working capital for businesses, especially SMEs.

Expected Benefits

- For Consumers:

- Increased disposable income, enhancing demand for goods and services.

- Reduced litigation due to simplified classification.

- For Businesses:

- Lower compliance burden, promoting ease of doing business.

- Potential rise in investment due to predictable tax environment.

- For Government:

- Streamlined revenue inflow through reduced evasion.

- Enhanced efficiency in tax collection via harmonised slabs.

Challenges and Concerns

- Incomplete IDS Resolution: Certain sectors (fertilisers, textiles, bicycles) continue to suffer from blocked credit.

- Revenue Concerns: Excessive rate cuts could limit fiscal capacity of the government.

- Frequent Changes: Continuous modifications in slab rates may cause uncertainty for businesses.

More Articles