9th September 2025 (14 Topics)

1

Sep

2

Sep

3

Sep

4

Sep

5

Sep

6

Sep

8

Sep

9

Sep

10

Sep

11

Sep

12

Sep

13

Sep

15

Sep

16

Sep

17

Sep

18

Sep

19

Sep

20

Sep

22

Sep

23

Sep

24

Sep

25

Sep

26

Sep

27

Sep

29

Sep

30

Sep

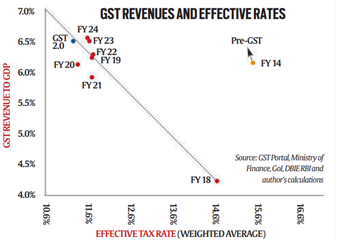

GST 2.0 Framework

Context:

The Union Government is moving towards GST 2.0 with an emphasis on simplification, long-term revenue growth, reduced compliance burden, and increased taxpayer participation.

Background of GST:

- Goods and Services Tax (GST) was launched on July 1, 2017, as India’s largest indirect tax reform.

- It subsumed multiple central and state-level taxes (excise, VAT, service tax, etc.) into a unified tax framework.

Current Issues with GST (GST 1.0):

- High compliance costs for businesses, especially MSMEs.

- Complexity due to multiple tax slabs (5%, 12%, 18%, 28%).

- Frequent procedural changes leading to uncertainty.

- Revenue challenges for states, often requiring compensation cess.

GST 2.0 – Proposed Features:

- Simplification: Reduction of tax slabs and streamlined processes.

- Lower effective tax rate: Estimated to decline from pre-GST 15.3% to about 11.4%.

- Compliance easing: Simplified return filing for small taxpayers, technology-driven monitoring, and dispute resolution via the GST Appellate Tribunal.

- Broader base, higher collection:Formalisation of the economy and wider taxpayer participation to sustain revenue growth.

- Digital integration: Use of GSTN (Goods and Services Tax Network) and e-invoicing for transparency.

Long-Term Goals:

- Achieve stable revenue buoyancy through broader participation rather than high tax rates.

- Align India’s tax system with global best practices.

- Ensure fiscal federalism by addressing state revenue concerns.

Economic Implications:

- Encourages voluntary compliance and lowers litigation.

- Enhances “ease of doing business.”

- Helps in formalising India’s largely informal economy.

More Articles